May 12, 2026

“The Final Phase of Elon’s Master Plan”?

FEATURED: NVDA Reports May 20

Editor’s Note: What is the final phase of Elon Musk’s master plan – and why could it mean a massive payday for anyone taking advantage of this ONE ticker? Our friend Larry Benedict, a hedge fund legend who made over $274 million for his clients, says he has the answer. Click here to see the details.

Dear Reader,

After PayPal. After Tesla. After SpaceX.

Elon Musk is now preparing to execute the final phase of one of the most ambitious plans in history.

Click here to discover exactly what he’s planning – and the ONE ticker that could benefit the most.

According to Larry Benedict – the man who delivered a 279% return on cash in 2025 while the S&P returned just 15% – when the “Final Phase of Elon’s Master Plan” is triggered, it could move more money than anything Elon has ever done before.

We’re talking billions – potentially trillions – of dollars flowing into a single ticker.

It’s not Tesla. It’s not SpaceX. It’s not crypto, or AI, or anything Wall Street is currently talking about.

But when the “Final Phase” kicks in, Larry believes it’s positioned to capture the surge.

He’s revealing the name and ticker today – completely free.

Regards,

Lauren Wingfield

Managing Editor, The Opportunistic Trader

NVDA Reports May 20: What the Numbers Say

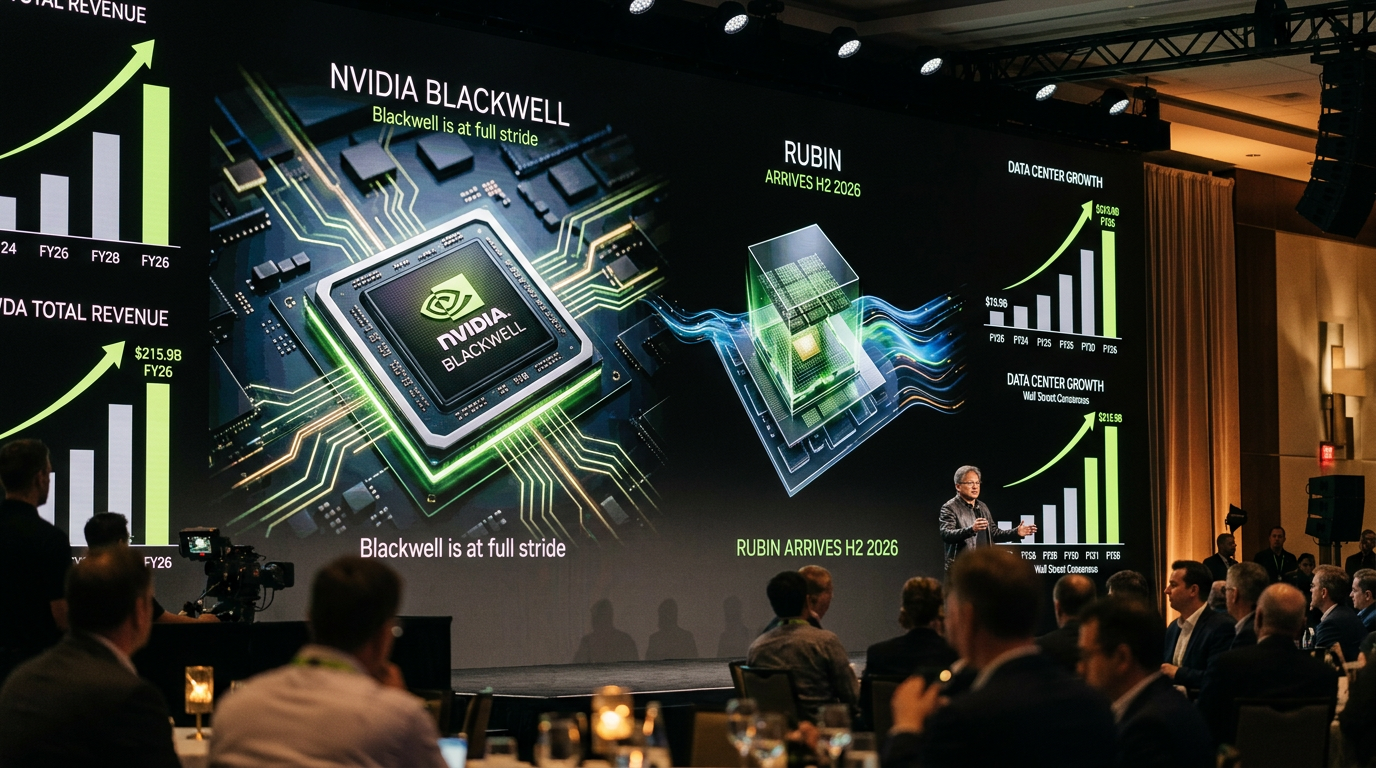

Nvidia reports fiscal Q1 2027 results after the close on May 20. The buildup has been unusually loud — and for once, the underlying data supports the noise.

This is a business that generated $215.9 billion in total revenue during fiscal 2026, up 65% year over year. Data center alone accounted for $197.3 billion of that — up from $115.2 billion the prior year. Q4 FY2026 came in at $68.1 billion in revenue, beating the $66.2 billion Wall Street estimate, with GAAP gross margins recovering to 75%. The company then guided Q1 FY2027 at $78 billion — which itself landed above what analysts had been modeling at the time.

Analyst Targets Heading Into May 20

- Goldman Sachs — Buy, $250 price target; expects a beat-and-raise quarter, with internal estimates 14–34% above broader Wall Street consensus through FY2027

- Susquehanna (Christopher Rolland) — Buy, raised to $275 from $250; cites surging hyperscaler capex and combined Blackwell/Rubin revenue potentially exceeding $1 trillion through 2027

- Consensus (38+ firms) — Strong Buy; median 12-month price target of approximately $265–$267, implying roughly 20–24% upside from current levels near $220

- High/Low range — Tigress Financial at $360 (high); consensus low at $210

The SpaceX IPO Could Move More Than Just Stocks

When major IPOs hit Wall Street, money doesn’t just flow into new shares.

Funds rebalance. Institutions reposition. Retirement accounts often move with them whether investors realize it or not.

A new free 2026 Gold Guide explains how some Americans are moving part of their retirement savings into physical gold tax-free and penalty-free.

Company Background

Nvidia is the dominant supplier of AI accelerators globally, holding over 90% market share in data center GPUs. Its competitive position rests on two pillars: hardware and CUDA — the proprietary software platform it introduced in 2006 that has since become the industry standard for AI development. With over 4 million developers building on CUDA and deep integration into every major AI framework including PyTorch and TensorFlow, switching costs are substantial. It’s not just hardware the customers are buying — it’s an entire development ecosystem built over nearly two decades.

Revenue breaks down across four segments: Data Center (now over 91% of total sales), Gaming, Professional Visualization, and Automotive. The company is, in practice, an AI infrastructure business. Gaming still matters at the margin — but data center is the whole game.

The Q1 FY2027 Numbers to Watch

Wall Street consensus is currently at approximately $78.8 billion in revenue and $1.78 EPS for Q1 FY2027. Management’s own guidance was $78 billion — representing roughly 77% year-over-year growth. Some estimates have moved higher since guidance was issued; ChartMill’s consensus now shows $80.1 billion in revenue and $1.79 EPS. The divergence matters: if the bar has quietly shifted to ~79–80% growth, a result that merely hits the company’s own $78 billion target may not generate much enthusiasm.

Key metrics the market will focus on:

- Data center revenue: Q4 FY2026 was $62.3 billion (+75% YoY). Analysts expect Q1 to continue that trajectory; Q1 FY2026 data center was $39.1 billion — the YoY comparison is straightforward and favorable

- Gross margin: Management guided GAAP gross margins of ~74.9% and non-GAAP at ~75.0% for Q1 FY2027. Full-year FY2026 came in at 71.1% GAAP / 71.3% non-GAAP. The sequential improvement is the story

- EPS: Wall Street expects approximately $1.74–$1.79. Full-year FY2026 non-GAAP EPS was $4.77; FY2027 consensus is $8.34 — a near-doubling

- Q2 FY2027 guidance: Consensus is around $86.6 billion — representing roughly 85% year-over-year growth. This number will drive the post-earnings reaction more than the Q1 result itself

- Free cash flow: Nvidia generated $97 billion in free cash flow in fiscal 2026 and returned $41 billion to shareholders through buybacks and dividends. The company enters Q1 with $51.1 billion in net cash

One accounting note investors should track: beginning in Q1 FY2027, Nvidia will include stock-based compensation in non-GAAP financial measures. This will add approximately $1.9 billion to non-GAAP operating expenses and compress non-GAAP gross margin by roughly 0.1%. EPS comparisons to prior periods will not be apples-to-apples without adjusting for this change.

Why the Stock Has Room to Move

The hyperscaler capex data is the clearest forward signal. Microsoft announced $190 billion in planned AI capex for calendar 2026, well above the $154 billion Wall Street had been modeling. Meta raised its capex ceiling to $145 billion. Alphabet’s guidance reached up to $190 billion. Amazon has committed $200 billion. Morgan Stanley’s latest forecast puts combined capex among the five largest hyperscalers at approximately $805 billion in 2026 — representing nearly 80% growth year over year — followed by 39% additional growth to $1.1 trillion in 2027.

You don’t build $800 billion worth of AI infrastructure without GPUs. And at this scale, you don’t buy GPUs without Nvidia’s Blackwell. That’s the simple version of why forward estimates may still be conservative.

Valuation context: Nvidia’s non-GAAP EPS for FY2026 was $4.77, putting the stock at a forward P/E of approximately 40.5 on FY2026 earnings — a steep discount to its 10-year average P/E of 61.7. On FY2027 consensus EPS of $8.34, the forward multiple drops to approximately 23.8x. That’s actually the lowest NTM P/E among its closest peers. Broadcom trades at 31.3x. ASML at 36.1x.

Innovation: Blackwell Now, Rubin Next

Blackwell Ultra is the dominant architecture across customer categories right now, with the prior Blackwell generation also still seeing active demand. CFO Colette Kress confirmed on the Q4 call that Nvidia shipped its first Vera Rubin samples to customers in late February 2026 and remains on track for production shipments in the second half of this year.

The Rubin platform is a meaningful step up — not just a spec upgrade. Key specs compared to Blackwell:

- Up to 10x reduction in inference token cost vs. Blackwell

- 4x fewer GPUs required to train mixture-of-experts (MoE) models

- Up to 18x faster rack assembly and servicing due to modular, cable-free tray design

- First platform to offer Nvidia Confidential Computing at rack scale

- NVIDIA Spectrum-X Photonics switch systems delivering 5x improved power efficiency

Among the first cloud providers confirmed for Rubin deployment in H2 2026: AWS, Google Cloud, Microsoft Azure, and Oracle Cloud Infrastructure, alongside Nvidia cloud partners CoreWeave, Lambda, Nebius, and Nscale. OpenAI, Anthropic, Meta, and xAI have also committed to adopting the Rubin platform for training larger models and running long-context multimodal systems.

There is one wrinkle worth noting. TrendForce estimates Rubin’s share of Nvidia’s overall shipments in 2026 will come in around 22% — below earlier projections of 29% — due to challenges around HBM4 memory validation, cooling optimization, and interconnect transitions. Blackwell is expected to dominate at over 70% of shipments. Analysts describe any deferral as a timing issue rather than a demand problem. But that’s a distinction to watch on the May 20 call.

The China Overhang — Updated

Nvidia’s Q1 FY2027 guidance explicitly assumes zero China data center compute revenue. That has been the baseline since the U.S. government required export licenses for H20 shipments to China in April 2025, a policy change that forced a $4.5 billion inventory charge in Q1 FY2026 — the largest one-time export restriction impact in the company’s history.

The situation has partially evolved. CEO Jensen Huang confirmed at GTC 2026 that Nvidia received purchase orders for H200 chips from Chinese customers — ByteDance, Alibaba, and Tencent were cleared to purchase over 400,000 units combined — after receiving necessary clearances from both U.S. and Chinese authorities. The U.S. government subsequently implemented a 15% fee on those China sales, paid to the Department of Commerce as a condition of the export license. Analysts estimate reopened China access represents a $5 to $10 billion annual revenue opportunity. None of that is currently in guidance. If any China revenue materializes in Q1 or is incorporated into Q2 guidance, it’s pure upside to published estimates.

Bull / Base / Bear Scenarios

Bull case: Q1 revenue clears $80 billion, Q2 guidance comes in at $88–90 billion or above, and management updates its language around demand visibility beyond what’s currently modeled. Any positive commentary on China data center re-entry would add further. Gross margins holding in the 74–75% non-GAAP range would confirm the Blackwell ramp isn’t compressing profitability. In this scenario, forward EPS estimates for FY2027 move higher, and the valuation re-rates meaningfully from current levels.

Base case: Q1 revenue lands in the $78–80 billion range, Q2 guidance meets consensus near $86–87 billion, and gross margins hold. The reaction is muted — investors had already positioned for a solid result, and without a material upside surprise on guidance, the stock drifts. This is the scenario where the stock’s 15% year-to-date gain and elevated pre-earnings positioning work against a sharp move higher.

Bear case: Q1 revenue meets guidance but misses the ~$79–80 billion that parts of the market now expect, Q2 guidance comes in below $86 billion, or gross margins disappoint at the low end of the guided range. Any negative commentary on Rubin delays, hyperscaler capex sustainability, or China export complications could amplify the downside. Worth noting: post-earnings selloffs in Nvidia are not unusual even on beat quarters. Q4 FY2026 saw the stock rise initially and then quickly surrender most of those gains despite a top-and-bottom-line beat.

What to Watch On the Call

- Q2 revenue guidance vs. the $86.6B consensus — this is the single most important number of the evening

- Rubin production timeline — any update on H2 2026 deployment schedule and early customer demand signals

- China commentary — whether any H200 revenue appears in Q1 actuals or Q2 guidance

- Gross margin trajectory — management has targeted mid-70s; watch whether they reiterate that language

- Demand visibility language — Jensen Huang’s comments on combined Blackwell/Rubin revenue visibility through 2027 have been as influential as the reported numbers themselves

- Hyperscaler concentration — cloud providers accounted for just under 50% of data center revenue in prior quarters; any shift in that mix matters for how durable the demand base looks

Bottom Line

The fundamental case for Nvidia is not subtle. Hyperscalers are spending more on AI infrastructure than Wall Street projected at the start of the year — meaningfully more. Blackwell is in full production. Rubin is shipping samples with production launches confirmed for H2 2026. The company has $51 billion in net cash, generated $97 billion in free cash flow last fiscal year, and trades at a lower forward earnings multiple than most of its semiconductor peers despite dramatically higher growth.

The harder question is whether any of that is genuinely unknown to the market at this point. The stock is up 15% year to date. Expectations coming into May 20 are high — possibly higher than the stated consensus suggests. A result that meets guidance but doesn’t meaningfully exceed it may not move the needle upward. A result that beats revenue, raises Q2 guidance above the $86.6 billion bar, and delivers positive commentary on Rubin demand and China access would be a different story entirely.

Watch the Q2 guidance number above everything else. That’s where the real signal is on May 20.

For informational purposes only.