May 19, 2026

The Pattern That Has Predicted Every Market Crash… Including the Next One

Featured – GE Aerospace +1.5%: International Orders Are Doing the Heavy Lifting

The Pattern That Has Predicted Every Market Crash… Including the Next One

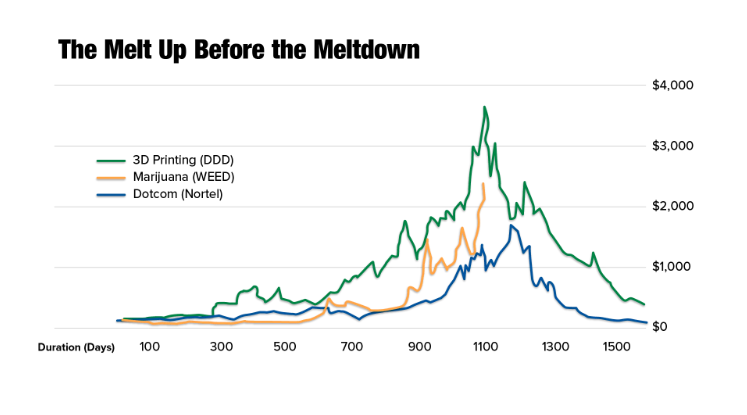

A sequence of events repeats throughout history.

Every bull market. Every bubble. Every crash.

The Great Depression, 1929. The dot-com bust, 2000. The financial crisis, 2008.

A former Goldman Sachs trader reveals the exact pattern that happens in every boom.

If you know the pattern, you can profit from it – and predict when to get out.

See his urgent presentation and learn the 3 steps to take now. Watch here.

Analyst Targets

- Morgan Stanley – Overweight | Target: $400

- Citigroup – Buy | Target: $353

- UBS – Buy | Target: $350

- Consensus (21 analysts) – Strong Buy | Avg. Target: $349

GE Aerospace +1.5%: International Orders Are Doing the Heavy Lifting

GE Aerospace (NYSE: GE) edged up +1.5% this session, and while that move might look modest on the surface, the underlying order flow supporting it is anything but. International demand for commercial turbine components – particularly through the CFM joint venture with Safran – has been building for months. The latest catalyst is a landmark U.S.-China aviation deal announced May 15, in which China agreed to purchase an initial 200 Boeing aircraft with the potential to expand to as many as 750 planes. Trump specifically cited GE Aerospace engines as part of the agreement. If the full order materializes, GE could supply 400 to 450 engines from the initial tranche alone – plus decades of high-margin maintenance contracts behind each one.

GE Aerospace CEO Larry Culp was part of the U.S. executive delegation accompanying President Trump to Beijing for the summit. That’s not a minor detail.

Company Profile

GE Aerospace is a global propulsion, services, and systems company operating through two primary segments: Commercial Engines & Services (CES) and Defense & Propulsion Technologies (DPT). It supports an installed base of approximately 50,000 commercial and 30,000 military aircraft engines worldwide. The services tail on each engine sale – repair, overhaul, spare parts, long-term agreements – is where the real economics live. Every new engine sold seeds a recurring, annuity-like revenue stream that can run for 20 to 30 years.

In at 9:35 AM. Out by 10.

I call it the “Opening Bell Breakout.” It’s the same setup I used to catch moves like 113% on GOOGL and 240% on META. I trade one simple 15-minute window each morning – and I’m usually done by 10 AM.

The Numbers

Q1 2026 was, objectively, a strong quarter – even if the stock’s initial reaction didn’t reflect that.

- Adjusted EPS: $1.86 vs. $1.60 consensus – a 16% beat, up 25% YoY

- Adjusted Revenue: $11.6B vs. $10.71B expected – up 29% YoY

- Total Revenue: $12.4B – up 25% YoY

- Free Cash Flow: $1.7B – up 14% YoY

- Total Orders: $23B – up 87% YoY (CES up 93%, DPT up 67%)

- Backlog: $211.3B – up from $190B at year-end 2025

- Operating Profit: $2.5B – up 18% YoY, well above $2.24B estimate

- Operating Margin: 21.8% – down 200 bps due to installed engine growth and inflation

- FY2025 Revenue: $45.86B – up 18.5% YoY

- FY2025 Adjusted EPS: $6.37 – up 38.5% YoY

Full-year 2026 guidance held at adjusted EPS of $7.10–$7.40 and free cash flow of $8.0–$8.4B, with management signaling it expects to finish toward the high end of both ranges. CFO Rahul Ghai noted Q1 came in roughly $300 million above internal expectations.

Why the Stock Is Moving

The +1.5% move today is primarily driven by the Chinese aviation deal and renewed international order momentum. Slight tangent, but worth noting: GE Aerospace also recently secured a 10-year maintenance and overhaul agreement with Japan Airlines for avionics systems support across its Boeing 787 fleet, serviced through Brisbane and Singapore. That deal compounds the international services picture quietly but meaningfully.

What the market is slowly pricing is this: GE isn’t just selling engines to China – it’s opening an aftermarket pipeline that could run for 30 years per aircraft. Boeing may win the headline, but GE collects on every departure.

The underlying Q1 data supports the optimism. LEAP engine deliveries surged 63% in the quarter. Internal LEAP shop visits were up over 50%. Commercial services revenue climbed 39%. These aren’t headline numbers – they’re the operating metrics that compound into long-range earnings power.

Macro Context

Global air travel demand remains structurally elevated. Airlines are accelerating narrowbody fleet expansion while simultaneously replacing aging aircraft – a dual demand cycle that puts intense pressure on engine manufacturers. GE’s CFM joint venture with Safran is the dominant supplier to that narrowbody replacement wave, powering both the Boeing 737 MAX and the Airbus A320neo. Emerging market growth in India and the Middle East is adding tailwind. The China reopening, if it holds, could be the most significant international catalyst for GE’s engine backlog since pre-pandemic fleet expansion.

The risk side of the macro picture is real, though. Elevated crude oil prices through Q3, softer global GDP projections, and Middle East conflict uncertainty all weigh on commercial aviation departures – GE’s primary volume driver. Management’s decision to hold guidance (rather than raise it) after Q1’s blowout quarter reflected that caution explicitly.

Wall Street is calling it the “Warsh Shock.” Here’s how to profit from it…

Nearly half of the world’s biggest money allocators are scrambling to reposition for what they expect to be the most volatile market in years.

Larry Benedict isn’t scrambling. He’s seen this before.

He says the Warsh Shock is setting up the most predictable wealth-building window he’s seen in 20 years… and there’s one ticker right at the center of it.

Forward Scenarios

- Bull: China order firms up at 750 aircraft with confirmed GE engine contracts. LEAP shop visit growth accelerates toward and beyond the 25% full-year target. Commercial services revenue runs ahead of the revised $4B YoY growth forecast. Stock re-rates toward $400 analyst targets on expanded earnings visibility.

- Base: China deal converts partially – 200 planes confirmed, balance uncertain. LEAP deliveries continue at elevated pace. Full-year 2026 EPS lands at the high end of $7.10–$7.40 guidance. Stock grinds toward consensus target of ~$349 on execution rather than multiple expansion.

- Bear: Geopolitical friction delays China deal formalization. Elevated oil prices suppress commercial departures in H2. Margin compression from installed engine growth and inflation widens. Stock remains range-bound with selling pressure on any guidance revision lower.

Technical Overlay

GE has been trading under pressure in recent weeks. The stock is currently sitting below its 20-day, 50-day, 100-day, and 200-day moving averages – and a death cross formed in May as the 50-day fell below the 200-day, reinforcing that the intermediate trend has been strained. Key resistance sits around $310, where overhead supply from the prior slide creates a clear ceiling. Support near $279–$280 is the level buyers have previously defended. Today’s +1.5% move on international order catalysts is constructive, but the technical structure still requires a fresh sustained catalyst to confirm a trend reversal rather than a short-term bounce.

What Investors Should Watch

- Formal confirmation of China Boeing aircraft deal terms and engine contract specifics

- LEAP internal shop visit growth vs. management’s 25% full-year target

- Commercial services revenue growth vs. the revised ~$4B YoY improvement forecast

- Any adjustment to FY2026 guidance at Q2 earnings (est. July 16)

- Geopolitical developments affecting Middle East departures and fuel availability

- Analyst price target revisions following the China deal announcement

Bottom Line

GE Aerospace’s core business is in excellent shape – a $211B backlog, four consecutive EPS beats, 87% order growth in Q1, and now a China pipeline that could extend demand visibility well into the next decade. The debate isn’t about whether the business is working. It’s about whether the stock, at ~35x forward earnings, can hold a premium multiple while macro headwinds compress near-term departure growth. The China deal is a legitimate long-term positive. Whether it’s enough to break the stock’s current technical weakness depends entirely on confirmation and delivery timelines – neither of which is settled yet.

For informational purposes only.