June 8, 2026

Inflation. Interest Rates. Frozen Jobs. Now This Chart.

Featured: AVO Earnings: What the Avocado Chain Is Telling Us

Something strange is happening in America.

You can feel it.

Inflation just hit 3.8% – the hottest reading in nearly three years, after climbing every single month of 2026.

The Federal Reserve’s benchmark rate sits at 3.50% to 3.75% – still more than double its pre-pandemic level – keeping mortgages, car loans, and credit-card APRs punishing for anyone borrowing.

And the labor market has frozen solid. 7.4 million Americans are out of work. One in four of them has been unemployed for more than six months. Payroll growth has essentially stalled over the past 12 months.

You feel it when the grocery bill outruns the raise. When the mortgage quote comes back and you close the tab. When your son sends out 80 résumés and hears back from two employers.

Most subscribers I talk to assume these are three different stories playing out at the same time.

They are not three different stories.

They’re three symptoms – of the same thing.

The same Tipping Point that has shaped every major technological shift in modern American history. The moment a small, committed minority of the S&P 500 crosses the 10% threshold – and the entire economy flips.

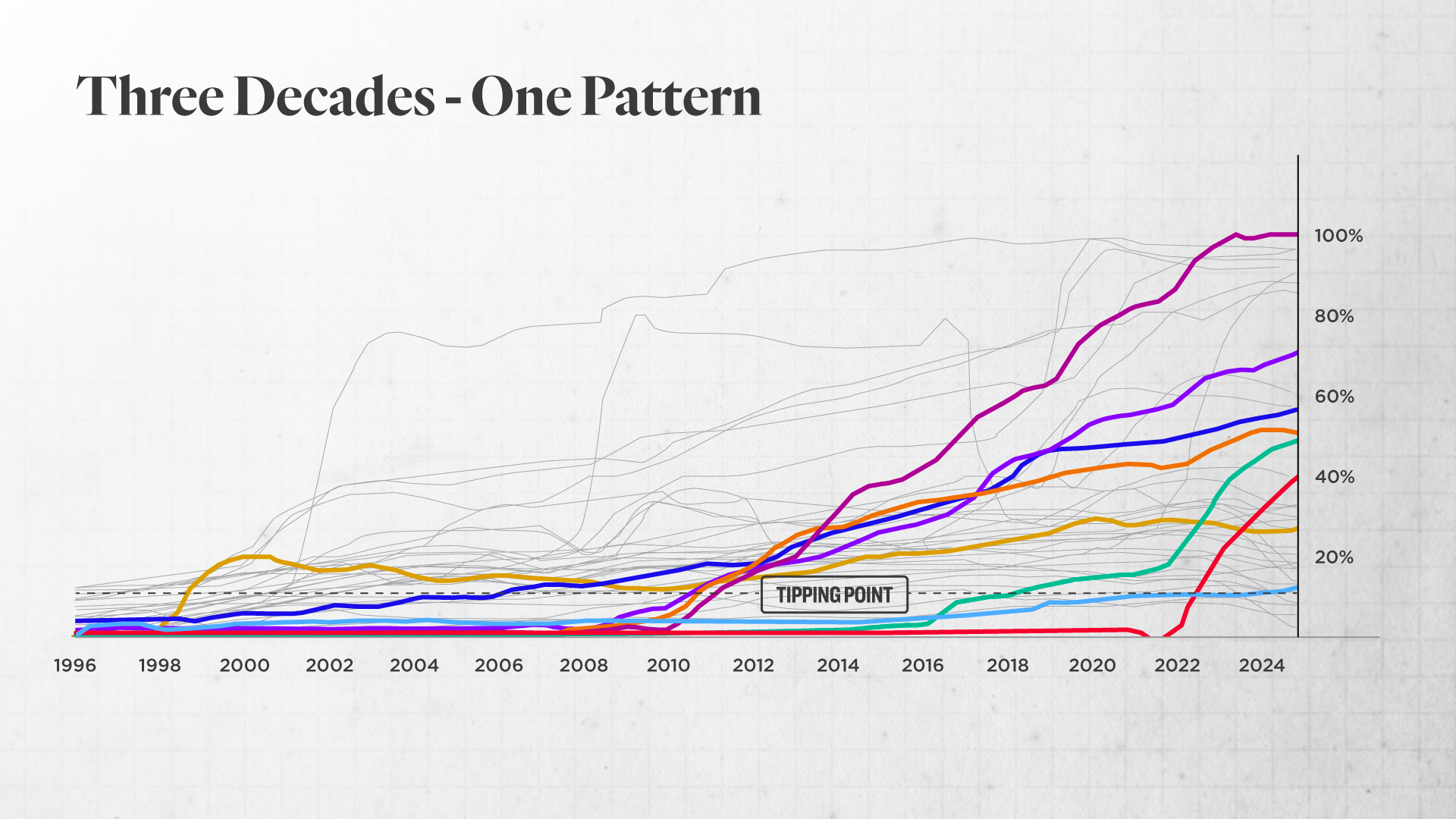

Look at the chart below.

Every line is a technology that mainstreamed across the S&P 500 in the past 30 years.

Every one crossed the same dashed line – the Tipping Point – before going vertical.

Look at the red line.

That is generative AI. Flat near zero from 1996 through 2021. ChatGPT launched in November 2022. The red line crossed the Tipping Point three months later – and by 2024, 40% of the S&P 500 was disclosing it in 10-K filings.

You watched the entire world change in 18 months.

Now look closer.

The pale blue line – the one easy to miss – just crossed the same Tipping Point.

And it is going to reorder what every prior crossing has reordered. Trillions in market value. Generations of winners and losers. Business models that looked indestructible six months earlier.

You are not imagining the strangeness. What you are feeling is the early stage of the cascade.

But here is what makes this one different – and why I believe this could be the last Tipping Point of its kind for a long, long time.

Morgan Stanley sizes the market at $5 trillion. McKinsey calls it “the most significant opportunity in a generation.” Sixty of America’s 500 largest companies are already disclosing it in their 10-K filings.

By every measure I have, this one absorbs the internet, the cloud, and AI infrastructure – and keeps going.

Once it is fully through, there is unlikely to be another wave like it for years – possibly decades.

I have put the entire story on film. The chart. The math. The three macro forces converging right now. And one company sits at the chokepoint through which every dollar of this transition has to flow.

This documentary tells you the stocks to buy. The stocks to sell. The three moves that put you and your family on the right side of the cascade.

It is all in the film.

Click here to watch the documentary now.

Good investing,

Porter Stansberry

AVO Earnings: What the Avocado Chain Is Telling Us

Analyst Price Targets

- Roth Capital: Buy | Price Target $17.00 (raised from $16.00, Sept. 2025)

- Stephens: Overweight | Coverage resumed 2026

- Consensus (2 analysts): Average 12-month target $17.50 | High $18.00 | Low $17.00

The avocado doesn’t get talked about as a supply chain stress test. It should be.

Tonight, Mission Produce (NASDAQ: AVO) reports its fiscal second quarter 2026 results after market close, hosting a conference call at 5:00 PM Eastern. The numbers will land in a market already jittery about fresh produce distribution economics, tariff exposure, and what Mexican oversupply is doing to per-unit pricing across the entire cold chain. Worth paying attention to – even if you don’t own the stock.

Company Profile

Mission Produce is a global Hass avocado distributor founded in 1983 and headquartered in Oxnard, California. The company sources, packs, ripens, and distributes fresh avocados – and increasingly mangoes and blueberries – to retail, wholesale, and foodservice customers across more than 25 countries. It operates through three segments: Marketing and Distribution, International Farming, and Blueberries.

What sets AVO apart structurally is vertical integration. The company owns five packing facilities across the U.S., Mexico, Peru, and Guatemala, with sourcing reach across 20-plus premium growing regions. That model gives it a tool that pure-play distributors don’t have: the ability to redirect fruit across geographies and customers in real time, which matters when one region’s harvest stumbles or pricing collapses in another. The company also just completed its acquisition of Calavo Growers in late May 2026, expanding its North American footprint and product mix – integration still underway, with at least $25 million in annualized cost synergies targeted within 18 months of close.

The Numbers Going In

Expectations for Q2 FY2026 are low. The Zacks consensus estimate pegs revenue at $269.3 million – a 29.2% decrease from the year-ago quarter – with EPS consensus at $0.07, down 41.7% from Q2 FY2025 actuals. Management already flagged that consolidated adjusted EBITDA will likely come in below the prior-year level due to margin and operating pressures.

Context matters here. In Q1 FY2026, AVO reported revenue of $278.6 million – down 17% year-over-year and short of the $319.6 million estimate – as a 30% pricing decline driven by Mexican oversupply overwhelmed a 14% volume gain. Gross margin still improved 190 basis points to 11.3%, and adjusted EBITDA rose 5% to $18.5 million despite the revenue drag. That combination – volume growing, margins holding, top line compressing – defines the current operating environment for the business.

For full context: FY2025 was the strongest year in company history. Record revenue of $1.39 billion, up 13% year-over-year. Volume of 691 million pounds of avocados sold. Adjusted EBITDA of $110.8 million, up 3%. Q4 FY2025 alone saw adjusted EBITDA hit $41.4 million, up 12% from the prior year. The FY2026 step-down in revenue is a function of pricing, not demand destruction.

Why the Stock Is Under Pressure

AVO is down roughly 21.8% over the past month heading into tonight’s report, trading near $12.56 against an average analyst target of $17.50. The market isn’t pricing in a business collapse – it’s pricing in an uncomfortable truth about commodity distribution: when prices fall hard and fast, even the best-run supply chain company feels it in the top line.

The core problem this quarter is single-origin sourcing dependency. Lower avocado prices are compressing per-unit margins specifically in a Mexican-dominant sourcing environment. Management also noted on the last earnings call that the California avocado harvest is running approximately one month later than last year, cutting sourcing flexibility and lowering utilization at the company’s California packing facilities. Those aren’t permanent structural problems – but they show up in a single quarter as meaningful cost and margin headwinds.

Slight tangent, but worth noting: AVO has a trailing four-quarter average earnings surprise of 126.5%. The market has been consistently too pessimistic on this company. Tonight could follow that trend – or the pricing compression cycle could finally catch up with the beat streak.

Macro and Industry Context

The broader supply chain picture for fresh produce is deteriorating in ways that favor incumbents with infrastructure – and punish lean distributors without it.

On the climate side, avocados are a water-intensive crop requiring roughly 320 liters per fruit. As temperatures rise and water scarcity worsens across Latin America, yields face real long-term pressure. The conditions already affecting production in regions like Mexico, Peru, and Chile are not hypothetical – they are current and compounding. In Mexico’s Michoacan state, the largest avocado-producing region in the world, production is expected to reach 9.2 million tonnes annually by 2028, but climate-driven cost increases and growing regulatory scrutiny are adding new overhead to growers and packers. As of January 2026, all Mexican avocados exported to the U.S. must come through deforestation-free supply chains – a compliance layer that adds cost and sourcing complexity for non-integrated distributors.

On the geopolitical side, tariff uncertainty has been a live variable. Management has been explicit about working around potential Mexican import tariffs, and the company’s global multi-origin sourcing model – Peruvian production, Guatemala operations coming online in the next 2-3 years – is built precisely for this kind of risk. Peruvian production has historically served as the backstop when Mexican volumes fluctuate, and that operational flexibility is a genuine structural advantage.

Bull / Base / Bear

- Bull: AVO beats a low Q2 bar on volume strength and margin discipline. Calavo integration proceeds cleanly, unlocking $25M-plus in synergies. Guatemalan supply coming online diversifies away from Mexico dependency. Stock closes gap to $17.50 analyst consensus over the next 12 months as pricing normalizes and FY2027 earnings growth of ~4% materializes. Vertical integration premium gets recognized.

- Base: Results roughly meet compressed expectations. Revenue comes in near $269M. Margins hold but don’t expand. Calavo integration creates short-term noise. Stock stays range-bound near current levels as investors wait for clearer FY2027 visibility. Capex declining toward $40M provides free cash flow support.

- Bear: Pricing deterioration is worse than guided. California harvest delay creates a second consecutive quarter of facility underutilization. Calavo integration costs exceed estimates. Revenue misses the $269M consensus, EBITDA falls materially below prior year, and the stock tests the 52-week low of $9.56. Tariff exposure on Mexican fruit becomes a near-term earnings risk that models haven’t fully absorbed.

Technical Overlay

AVO is trading near $12.56, down sharply from a 52-week high of $15.25 and sitting closer to the 52-week low of $9.56 than to analyst targets. The stock’s trailing P/E sits at approximately 23x with a forward P/E near 16x – suggesting the market is pricing in an earnings recovery but not betting heavily on it. A move toward the $17.00-$17.50 analyst target range would require either a material positive earnings surprise tonight or a shift in the pricing environment for avocados in the back half of fiscal 2026. Key levels to watch: $13.50 resistance from prior consolidation, and $10.50 as meaningful near-term support above the 52-week floor.

What to Watch on the Call Tonight

- Per-unit avocado pricing guidance for Q3 FY2026 – particularly whether the 30-35% pricing decline below $2.00/lb is stabilizing or accelerating

- Calavo acquisition integration update and initial synergy tracking

- Peruvian harvest volume outlook as a pricing offset to Mexican oversupply

- Guatemala packhouse contribution timeline

- Any tariff or trade policy commentary on Mexican sourcing

- FY2026 capex confirmation near $40M and free cash flow trajectory

Bottom Line

The debate on AVO isn’t really about avocados. It’s about what happens to a vertically integrated operator when commodity pricing drops 30% and the market mistakes a volume story for a margin collapse. Mission Produce has proven it can move fruit across geographies, absorb pricing cycles, and grow volume even when revenue compresses. The question tonight isn’t whether the business is broken – it isn’t. The question is whether the pricing environment has bottomed and whether the Calavo integration executes cleanly enough to give investors a reason to look past the near-term top-line pressure.

That’s what 5:00 PM Eastern is for.

For informational purposes only.