July 8, 2026

The Ceasefire Is Over. The Market Split in Two.

Featured: The Ceasefire Is Over. The Market Split in Two.

Dear Reader,

Tomorrow morning a small group of investors will get a text message…

From a secure app on their phone.

It could come as early as 9:30 a.m.

The app is a direct link to possibly the world’s most powerful stock rating software.

Every time it sent a message…

The average gain was 310%.

And that includes the times it missed.

The folks on this exclusive list have seen almost 3,000 chances to double their money…

And over 400 chances to 10x their money.

This next message could do the same thing…

But right now…

You won’t receive this text message.

Click here to learn how to sign up for these alerts

Chris Graebe

FEATURED

The Ceasefire Is Over. The Market Split in Two.

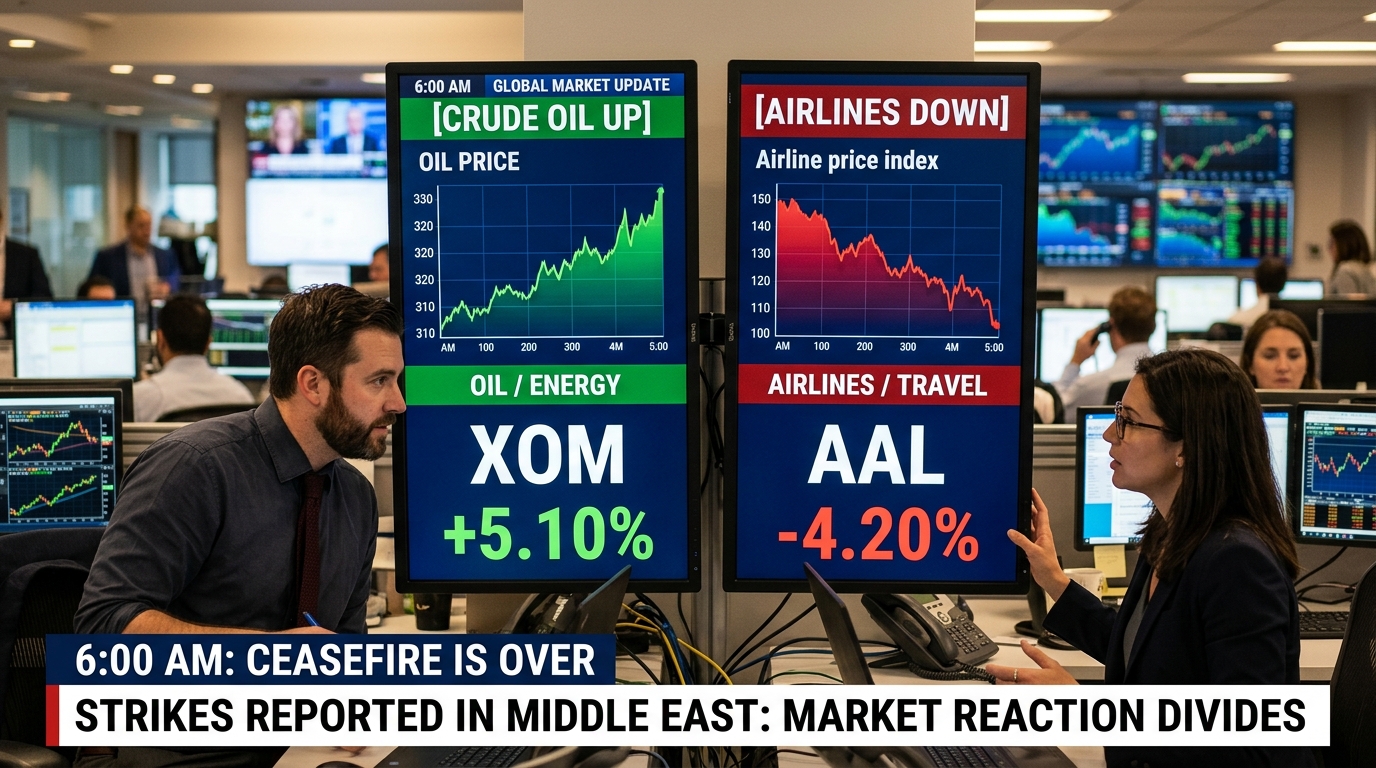

Trump said three words this morning that moved more money than any earnings report this quarter: “It’s over.”

Speaking on the sidelines of the NATO summit in Ankara, President Trump declared the US-Iran memorandum of understanding effectively dead, hours after American forces carried out a series of strikes against Iran and Tehran retaliated by targeting US military sites in Bahrain and Kuwait. The immediate market reaction was sharp, fast, and completely asymmetric.

Brent crude surged 5% to around $78 a barrel by mid-morning Wednesday. WTI jumped more than 5% to $74 per barrel, its largest single-day move higher since early June. Meanwhile, the Dow Jones Industrial Average fell 1.2%, shedding more than 600 points, while the S&P 500 dropped 0.6% and the Nasdaq gave up 0.5%.

What happened under the surface, though, is the more interesting story.

A Market Divided

This is not a broad selloff. It is a forced reallocation, and some investors are getting paid while others are getting punished in the same moment.

Chevron rose 2.8%, ExxonMobil gained 2.6%, and ConocoPhillips advanced 2.9% in early trading. On the other side, United Airlines dropped 4.2%, Southwest Airlines lost 3.3%, and Delta Air Lines fell 3.2%. Cruise operators also slipped, with Carnival down 3.1%, Royal Caribbean 3.2%, and Norwegian Cruise Line 2.5%.

The math here is brutally simple. Jet fuel costs move with oil prices, and they had already surged well ahead of the broader crude recovery since the Iran conflict began. Airlines had been hoping the MOU was the beginning of a path back to normal fuel costs. That hope is gone, at least for now.

Airline stocks have been behaving in binary fashion all year, surging on any credible de-escalation signal and reversing sharply the moment conflict headlines return. The sector’s earnings model is acutely sensitive to one input variable.

That one variable is jet fuel. And jet fuel just got more expensive again.

What the Market Had Already Accepted

Here’s the context that matters. After the US and Iran signed a memorandum of understanding in mid-June, US oil prices stabilized around $69 to $70 per barrel and held there for the better part of three weeks. Airlines had started to recover. Travel stocks were quietly building back. The market had essentially accepted a slow normalization of energy supply through the Strait of Hormuz.

One press conference unwound all of that.

“For markets and the global economy, the prospect of a swift return to pre-conflict energy and goods flows through the waterway is fading,” said Geoff Yu, senior market strategist at BNY.

Slight tangent, but it matters: this is the second time in under three months that a single Trump statement caused a multi-percent move in crude oil. The market has essentially been trading on one binary all year, open or closed. Today it moved back toward closed. Sharp swings in global oil prices have repeatedly reflected changing views on the likely duration of the conflict, with indications of a prolonged closure pushing oil up and headlines suggesting a quick resolution sending prices tumbling.

The Fed Problem Nobody Wants to Talk About

Oil prices re-accelerating creates a problem that extends well beyond energy stocks.

Elevated energy prices have already shifted investor expectations toward higher policy rates later this year, a sharp reversal from earlier bets on one or two rate cuts in 2026. The Fed held the federal funds rate unchanged at 3.50% to 3.75% for the fourth consecutive meeting in June under new Chair Kevin Warsh. New economic projections showed 9 of 18 officials see at least one rate hike this year, with 6 anticipating at least two. PCE inflation was revised sharply higher to 3.6% for 2026.

If Brent holds above $78 or pushes toward $80, the Fed’s already-complicated inflation math gets worse. Futures markets are currently pricing a path that rises to about 3.8% by October and approaches 4% by year-end. Higher rates are not what growth-heavy stocks want to hear right now. Which explains why chip stocks broadly sold off on Tuesday, with Micron down 4.7% and the VanEck Semiconductor ETF falling more than 3%, as energy and rate pressure combined with AI valuation concerns.

The sectors that benefit from lower rates, technology, high-growth software, speculative small caps, are getting squeezed from two sides. Energy inflation from below. Valuation compression from above.

Who Wins. Who Loses.

The energy supermajors are the clearest beneficiaries of re-escalation. ExxonMobil operates at massive scale, with upstream production hitting 4.6 million oil-equivalent barrels per day in Q1, and its large Permian Basin footprint keeps break-even costs well below current WTI levels. At $74 WTI, the margin spread is meaningful.

ConocoPhillips operates exclusively in upstream exploration and production, meaning its earnings are more directly tied to oil prices than an integrated major like Exxon. That concentrated model is a feature today, not a bug. Devon Energy climbed 2.5%, while Occidental Petroleum, APA Corp, and Diamondback Energy were up 2.5%, 3%, and 3.8%, respectively.

On the other side, the losers are predictable but the magnitude is not. Aviation has been significantly disrupted by the closure of key flight corridors between Africa, Asia, and Europe, with airlines rerouting along longer paths that circumnavigate the Middle East, adding journey time and fuel costs. Today’s re-escalation puts that disruption premium back on the table after three weeks of relative calm.

Worth noting: IATA has already cut its 2026 global airline profit outlook to roughly $23 billion, down from an earlier $41 billion forecast, with rising fuel costs as the primary driver. That estimate was made before today’s move in oil.

The Technical Picture

WTI crude had been range-bound between roughly $68 and $72 for most of late June and early July. Today’s move to $74 breaks the top of that range on significant volume. If Brent holds above $78, the next area traders are watching is the $82 to $84 range. A sustained move there would meaningfully change the earnings math for airlines, cruise lines, and any fuel-intensive business that had already assumed supply normalization.

For energy equities, XOM, CVX, and COP all remain well below their spring highs. Brent peaked near $121 in late April at the height of the Hormuz disruption. There is room to run if the conflict re-intensifies, but also significant downside if another ceasefire materializes. The trade is binary, and it always has been.

What Investors Should Watch

- Strait of Hormuz shipping data — tanker traffic is the real-time indicator of whether this is a 24-hour event or a structural re-escalation. Before the conflict began, about 20% of global energy supply passed through the strait. Any resumption of that flow changes everything.

- Fed communications and July FOMC signals — the July 28-29 meeting is approaching. Watch for any language suggesting the Fed views renewed energy inflation as a trigger for additional tightening. June CPI data lands July 14 and will be closely read.

- Airline fuel hedging disclosures — Delta, United, and Southwest have all been managing fuel exposure differently. The degree to which they are hedged determines how much of today’s oil move actually hits Q3 earnings. Delta reports Q2 results on July 10.

- Treasury license status — the US revoked the waiver that allowed Iran to sell crude following the Hormuz attacks. If that revocation holds, Iranian supply is effectively off the global market again, which is a structurally bullish signal for crude.

The Bottom Line

The market spent three weeks accepting a world where the Strait of Hormuz slowly reopened. One sentence from Trump this morning asked it to unwind all of that.

The real question is not whether energy stocks go higher today. They probably do. The real question is whether this is a 48-hour news cycle or the beginning of a second leg of the conflict that derails the second half of 2026’s earnings recovery.

Both things can be true at once: energy wins short term, and the broader market loses medium term, if this holds. The latest escalation puts pressure on an equity rally that was already showing signs of fatigue, with higher oil prices threatening to revive inflation concerns and further complicate the Fed’s path forward.

The spread between XOM and UAL today tells you everything. One sentence. Two completely different portfolios. The market has not decided which one is right yet.

For informational purposes only.